Analysing the Income Tax table is crucial for those who will be filing this year. Be sure to check out the income tax rates for 2023.

- To understand the income tax table, the concepts involved are relatively simple.

- The calculation basis is made up of the taxable income received in the previous year, after adding up all taxable income and subtracting the deductions allowed by law, such as health and education expenses.

- The rate is the percentage of the tax base, calculated according to the progressive income tax table or fixed rate, depending on the type of income.

- The deductible portion is a fixed amount that can be deducted from the tax base, reducing the amount to be paid.

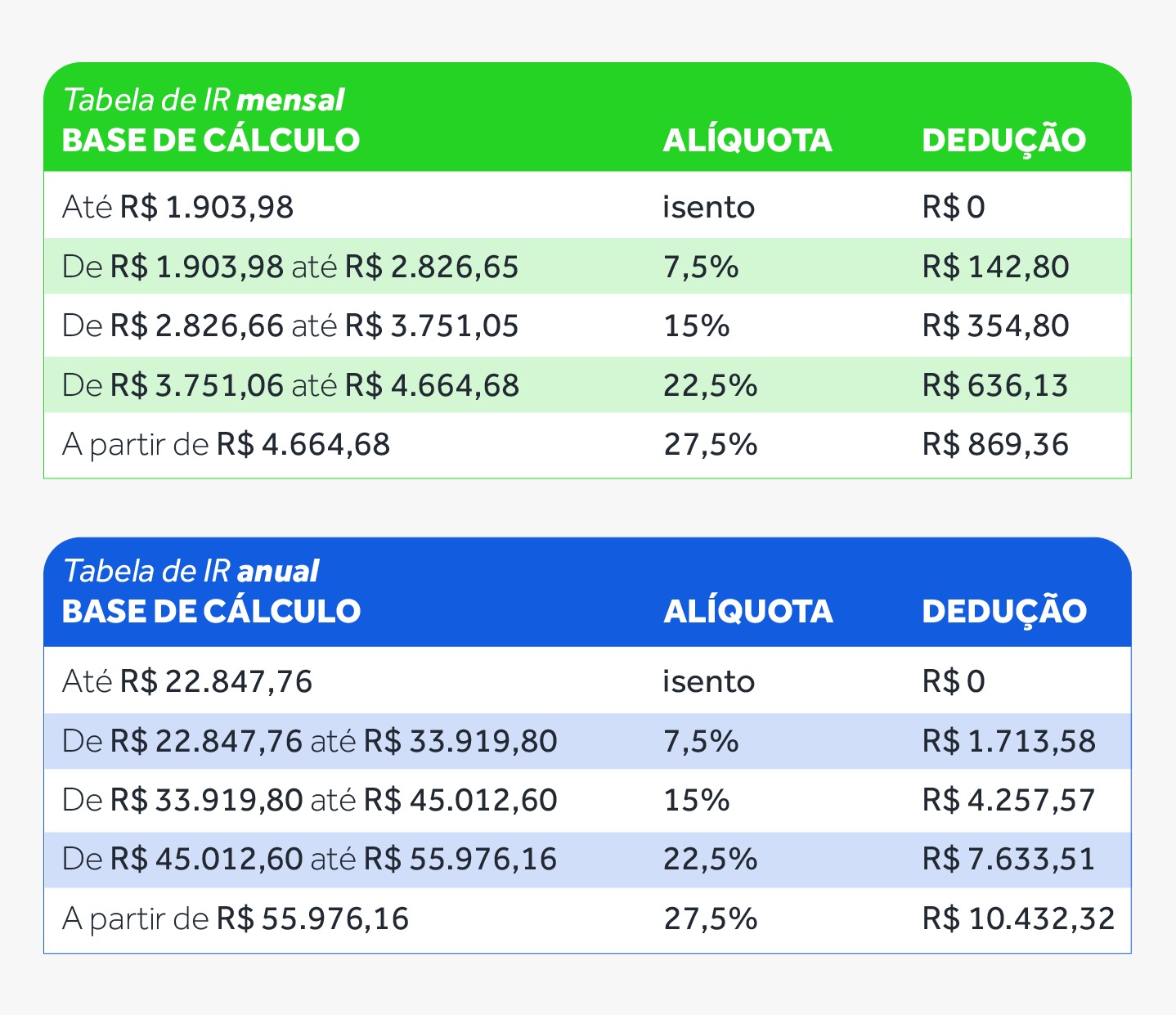

The income tax table varies according to the taxpayer's monthly income, and the higher the income, the higher the percentage rate applied to income.

Professionals responsible for companies' personnel departments must be familiar with the Income Tax table in order to calculate the tax that must be passed on to the public coffers. This is because employers are responsible for withholding part of employees' salaries based on the progressivity of the income tax table.

It's important that taxpayers also keep track of the amounts deducted from their salaries on a month-by-month basis, so that they can better organise their finances and invest in opportunities in the market. It's worth pointing out that the IRS has been using the same data since 2015, which means that if you already know how to file your income tax return, you're probably used to the rates and percentage variations. However, it's always good to be aware of updates and changes to the table to avoid future problems with your tax return.

Here's how to calculate income tax in 2023:

After understanding the importance of the Income Tax table as a basis for calculating the amount to be paid, it is essential to understand how to apply the corresponding percentage. This is especially relevant for workers who want to better understand the deductions on their payslips.

Having the correct data is essential for calculating income tax. Information such as

- The value of the gross salary

- The deduction for expenses

- The deduction for dependents

- INSS calculation multiplied by the rate

Income tax withheld at source = [(Gross salary - dependents - INSS) X rate] - deduction

One important piece of information to note is that if you have dependents declared on your income tax return, you can obtain a deduction of R$2,275.08 from the total amount of tax due for each dependent.

What is the deadline for filing the Individual Income Tax Return 2023?

It's essential to be aware of the deadline for filing your personal income tax return (IRPF), as well as the tax rates. In 2023, the Federal Revenue Service has set the deadline to begin on 15 March and end on the last second of 31 May.

These times are based on the Brasilia time zone. It is advisable not to leave the declaration to the last day, as system overload and the possibility of forgetting documents can cause problems and cause you to miss the deadline.

It is essential to prepare in advance and send in your tax return without any errors or omissions, as taxpayers who send in their tax return early have priority in receiving their refund.

However, if you miss the deadline, you could fall into the fine mesh and receive a fine ranging from 1% of the tax amount to a maximum of 20% of the tax.

It is important to note that priority for restitution is also given to the elderly, people with serious illnesses and the physically or mentally disabled, as long as the legal requirements are met.

In 2023, income tax refund dates will be divided into five batches

Check out the dates for each batch below:

- 1st batch: 31 May 2023.

- 2nd batch: 30 June 2023.

- 3rd batch: 30 July 2023.

- 4th batch: 31 August 2023.

- 5th batch: 29 September 2023.

Important to remember that taxpayers who submit their tax returns early and without errors will be prioritised for tax refunds. However, priority will be given to:

- Elderly

- People with serious illnesses and physical or mental disabilities

- Taxpayers whose main source of income is teaching

- Taxpayers who used the pre-filled declaration and/or opted to receive the refund by Pix.

As provided by law.

Do you know what information is needed to file your income tax return?

The declaration must contain all financial information relating to the base year, such as income received from individuals and companies, capital gains, movable and immovable property, debts and liens, among others.

It's important to remember that all information must be declared accurately and transparently to avoid errors and, consequently, the need to rectify the declaration later. In addition, it is essential to keep proof of all the information declared

To declare your income for income tax purposesIn the case of a tax return, it is necessary to present documents known as income reports, which are provided by three different sources:

- The employer,

- Your bank account

- And the stockbroker you invest with

The employer's income report proves the worker's income throughout the year and must be provided by 28 February.

The purpose of the bank's income report is to present bank transactions throughout the year, while the broker's report presents the investments made and the gains achieved on the investments, including the corresponding taxation.

To make the tax return process easier, it's important to organise yourself throughout the year and keep all your receipts. In addition, maintaining personal financial control is fundamental to achieving your goals and having a promising future.

We also recommend checking out specific content to find out how:

- Declare actions

- CBD,

- Investment funds,

- BDRs, LCI and LCA,

- Savings, direct treasury,

- Dividends and income.

Did you know that you can reduce the amount of income tax you have to pay by up to 12%? That's right!

And one of the ways to get this discount is by investing in a Free Benefit Generator Plan (PGBL), a type of private pension scheme.

By investing in a PGBL, you can deduct up to 12% from your taxable income for the previous year, which results in a reduction in the total amount of tax to be paid.

If you opt for the full PGBL declaration instead of the simplified one, you can unlock more than R$2,500 of your income tax refund.

What can you deduct from your income tax?

In addition to declaring your income, you can also include expenses and outgoings in order to deduct them from your income tax bill. The IR deduction is a way for taxpayers to get a discount on the amount to be paid, since the IRS considers that part of the tax has already been paid.

In order for an expense to be eligible for tax deduction, you need to provide proof that contains personal information, such as name and CPF, as well as the details of those responsible for the service, whether they are individuals or companies.

See below which expenses can be deducted from your income tax:

Health expenses: health expenses are common in income tax returns. If you've spent money on health insurance, exams, a dentist, a psychologist, a physiotherapist, a speech therapist, a hospital, among other health-related expenses, you may be able to deduct them from your tax bill. There is no limit to the number of expenses you can include in this category, i.e. you can include all your expenses for these services, as long as you have proof.

Education expenses: if you spend on your children's college or school, you can get an income tax deduction for these expenses. This category of expenditure has a limit of R$3,561.50 per person and only expenditure on formal education is valid. In other words, this includes spending on early childhood education (nursery and pre-school), primary education, secondary education, higher education (undergraduate and postgraduate) and professional education (technical and technological education).

Deduction for dependents: if you have dependents declared for income tax, you are entitled to deduct R$2,275.08 per dependent.

Income tax deduction for alimony: taxpayers who pay alimony can deduct the full amount from their income tax. It is important to note that this rule only applies to situations in which there is a court agreement to define the amount.

Deduction for official and private pensions: taxpayers who have part of their salary withheld to pay the INSS can deduct the amount when paying tax. If you have a Free Benefit Generator Plan (PGBL) or an Individual Programmed Retirement Fund (Fapi), you can deduct 12% from your income tax for the year. In the case of the PGBL, this deduction is only valid if you also contribute to the official pension scheme.

That you have to declare and pay income tax

A Inland Revenue sets the rules to define the obligation. For the 2023 Income Tax, they must declare:

- Taxpayers with taxable income above R$ 28,559.70 in 2022.

- Taxpayers with exempt income above R$ 40,000.00 in 2022.

- Those who carried out transactions on the Stock, Commodities, Futures and Similar Exchange totalling more than R$ 40,000 in 2022.

- Citizens who made a capital gain on the sale of assets or traded on the Stock Exchange in 2022.

- Those who chose the tax exemption on the sale of residential property for the purchase of another property within 180 days in 2022.

- People who had annual gross revenue of more than R$ 142,798.50 from rural activities in 2022.

- Those who want to offset losses relating to rural activities carried out in previous years.

- Those who had possessions totalling more than R$ 300,000 on 31/12/2022.

- All people who became resident in Brazil in any month of 2022.

Who doesn't need to file an income tax return?

Contrary to what many people think, the The obligation to pay income tax is not just based on specific parameters. The IRS also establishes some situations in which taxpayers do not need to declare the tax.

For example, people with monthly income below the minimum amount required for the income tax return (currently R$1,903.98) do not need to declare. Likewise, taxpayers over 65 who are retired and depend exclusively on their pension are also exempt.

Another situation is when someone is declared as a dependent in another declarationThis means that you are exempt from income tax. However, it is necessary to submit an income declaration so that the government can verify the income of the person you depend on.

Finally, taxpayers suffering from certain serious illnesses, such as:

- AIDS

- Severe heart disease

- Blindness

- Parkinson's disease and others

They can apply for income tax exemption by presenting a medical report proving the illness.

CONCLUSION:

It's important to remember that although many people believe that only those who fall within certain parameters need to declare their income tax, the IRS also establishes cases in which taxpayers are exempt. This is the case for people with a monthly income of less than the minimum amount to declare income tax, taxpayers over 65 who are retired and live solely on their pension, people declared as dependents and those with listed illnesses who can apply for tax exemption with a medical report.

However, even if you are exempt from Income Tax, it is important to bear in mind that in some cases you still need to declare your income so that the government can cross-check the data and analyse the income of the person you depend on. In addition, it's worth noting that the deadline for filing the 2023 Income Tax return is 30 April and that if you are obliged to file, it's important to pay attention to the rules and criteria defined by the Receita Federal to avoid future problems.